HFW 19: Automate ETS

AutoETS improves forecasts meaningfully vs. ETS on Apple

In our last post, we introduced the ETS model, which is an exponential smoothing model for Trend and Seasonality that includes an Error term, hence ETS. Why it isn't called TSE, rather than ETS since the error innovation only came later, is anyone's guess. Whatever the case, employing this model saw a modest improvement in performance relative to the naive and autoregressive growth (AR1(%)) benchmarks. It also outperformed the simple exponential smoothing (SES) model, though the differences were minor.

Having set up the ETS model, we can now introduce AutoETS, which is simply an automated way to select the best parameters from the nine different combinations of error, trend, and seasonality that are either additive or multiplication. We were remiss to mention in our prior post that the ETS model was originally developed in couple of key papers from 1997 and 20021 and covered in detail in a book by the great Rob Hyndman and others: Forecasting with Exponential Smoothing: The State Space Approach. Recall, ETS models are referred to as innovations state space models where "state space" comes from multiple equations: one that describes the observed data and the others that describe how the other components—level, trend, or seasonality, in other words, states—change over time. The "innovations" part is that all equations use the same random error process.

That's enough history. Time for us to stand on the shoulders of giants. Before we do, we should first explain some terminology. When folks discuss a particular ETS model you might see something like ETS(NAM). The letters inside the parentheses stand for None, Additive, and Multiplicative aligning with Error, Trend, and Seasonality. Hence, the model we showed in our last post was an ETS(AAA) model, as each of the states was assumed to be additive (More on additive vs. multiplicative in a later post). AutoETS finds the best configuration of those nine possible combinations of ETS and NAM.

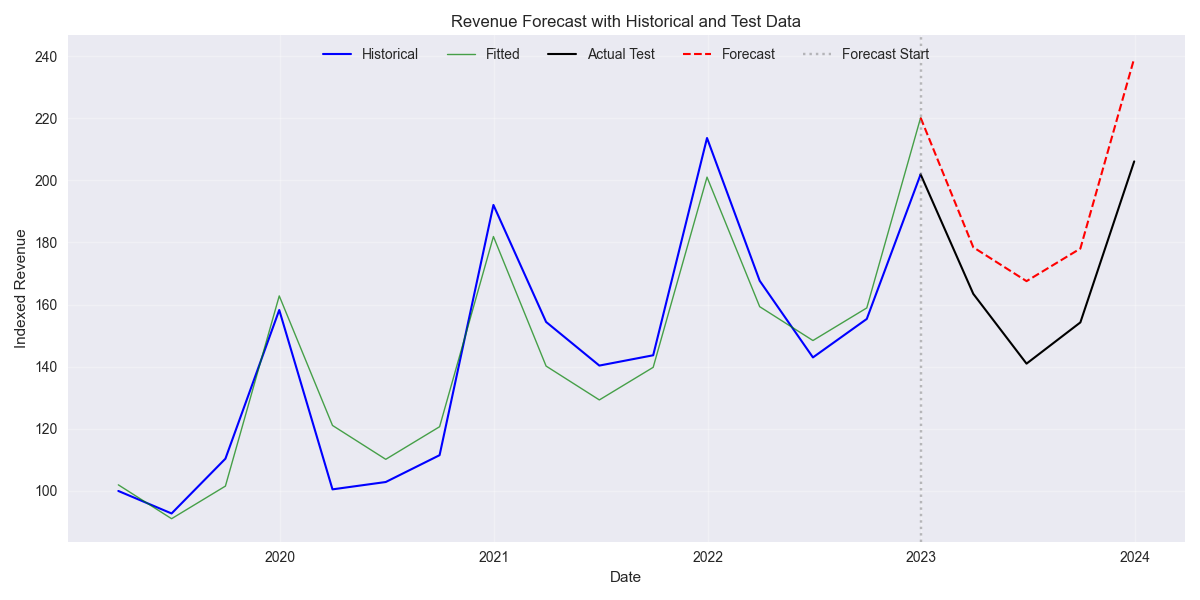

Before we deploy AutoETS on our data set in the next post, we’ll look at single example where we compare an ETS(AAA) model from our last post to an AutoETS model on Apple. Let's go!

In the first graph, we show the ETS(AAA) model with the fitted values on the training set and the forecast values. As one can see, the fitted values follow the shape of Apple's revenues nicely. The forecast looks pretty good too. Recall, one of the reasons one might favor an SES or ETS model over a naive one, even if the naive's error rate is lower, is that the forecasts actually look like forecasts. In any case, the root mean-squared error (RMSE) for the ETS(AAA) model is about 25 (which doesn’t really tell you much) and the scaled RSMSE is 15%. In other words, the RMSE of the forecasts is a fraction of average actuals. That's pretty good given that the aggregate scaled RMSE for XLK has tracked the 70-80% range out of all the different models we've tried. Of course, that is mainly due to the inclusion of Nvidia.

Let's see what AutoETS can do. We only show the forecasts for ETS(AAA) and AutoETS below.

Clearly, AutoETS follows the actual revenues in the test much more closely. Critically, the scaled RMSE for the AutoETS model is only about 5%, a 66% reduction in error! (Don't you love when you can use the change in percentages to make a dramatic point!) Plus one for the AutoETS model. Of course, this is only one instance. But we are curious to find out what AutoETS decided were the best parameters. It turns out it was an MNA model, or, in other words Multiplicative Errors, No Trend, and Additive Seasonality.

We'll look at this in more detail as well as the mechanics of putting the Auto in AutoETS. But for now this is an encouraging development and we're looking forward to seeing how AutoETS performs on the full dataset. Stay tuned!

Code below.

# Load packages

import numpy as np

import pandas as pd

from datetime import datetime, timedelta

import statsmodels.api as sm

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormatter

import matplotlib as mpl

import pickle

from statsmodels.tsa.exponential_smoothing.ets import ETSModel

from sktime.forecasting.ets import AutoETS

# Assign chart style

plt.style.use('seaborn-v0_8')

plt.rcParams["figure.figsize"] = (12,6)

# Handy functions

# Functions to load and save files

def save_dict_to_file(data, filename):

with open(filename, 'wb') as f:

pickle.dump(data, f)

def load_dict_from_file(filename):

with open(filename, 'rb') as f:

return pickle.load(f)

# Create functions for indexing

def create_index(series):

if series.iloc[0] > 0:

return series/series.iloc[0] * 100

else:

return (series - series.iloc[0])/-series.iloc[0] * 100

# Function for scaled RMSE

def get_rmse_scaled(series):

return np.sqrt(np.mean((series['actual']-series['predicted'])**2))/np.mean(series['actual'])

# Function to flatten

def flatten_df(dataf: pd.DataFrame, group_name:str, cols:list) -> pd.DataFrame:

df_grouped = dataf.groupby(group_name)[cols].agg(list)

for col in cols:

df_grouped[col] = df_grouped[col].apply(lambda x: np.concatenate(x))

df_long = df_grouped.apply(pd.Series.explode).reset_index()

return df_long

# Symbols used

etf_symbols = ['XLF', 'XLI', 'XLE', 'XLK', 'XLV', 'XLY', 'XLP', 'XLB', 'XLU', 'XLC']

ticker_list = ["SHW", "LIN", "ECL", "FCX", "VMC",

"XOM", "CVX", "COP", "WMB", "SLB",

"JPM", "V", "MA", "BAC", "GS",

"CAT", "RTX", "DE", "UNP", "BA",

"AAPL", "MSFT", "NVDA", "ORCL", "CRM",

"COST", "WMT", "PG", "KO", "PEP",

"NEE", "D", "DUK", "VST", "SRE",

"LLY", "UNH", "JNJ", "PFE", "MRK",

"AMZN", "SBUX", "HD", "BKNG", "MCD",

"META", "GOOG", "NFLX", "T", "DIS"

]

xlb = ["SHW", "LIN", "ECL", "FCX", "VMC"]

xle = ["XOM", "CVX", "COP", "WMB", "SLB"]

xlf = ["JPM", "V", "MA", "BAC", "GS"]

xli = ["CAT", "RTX", "DE", "UNP", "BA"]

xlk = ["AAPL", "MSFT", "NVDA", "ORCL", "CRM"]

xlp = ["COST", "WMT", "PG", "KO", "PEP"]

xlu = ["NEE", "D", "DUK", "VST", "SRE"]

xlv = ["LLY", "UNH", "JNJ", "PFE", "MRK"]

xly = ["AMZN", "SBUX", "HD", "BKNG", "MCD"]

xlc = ["META", "GOOG", "NFLX", "T", "DIS"]

sectors = [xlf, xli, xle, xlk, xlv, xly, xlp, xlb, xlu, xlc]

# Sector dictionary

sector_dict = {symbol.lower(): tickers for symbol, tickers in zip(etf_symbols, sectors)}

sector_map = {ticker.lower(): symbol for symbol, tickers in zip(etf_symbols, sectors) for ticker in tickers}

# Load data from disk

# See Code Walk-Throughs for how we built the data set

df_sector_dict = load_dict_from_file("path/to/data/simfin_df_rev_dict.pkl")

# Clean dataframes

df_rev_index_dict = {}

for key in sector_dict:

temp_df = df_sector_dict[key].copy()

col_1 = temp_df.columns[0]

temp_df = temp_df[[col_1] + [x for x in temp_df.columns if 'revenue' in x]]

temp_df.columns = ['date'] + [x.replace('revenue_', '').lower() for x in temp_df.columns[1:]]

temp_idx = temp_df.copy()

temp_idx[[x for x in temp_idx if 'date' not in x]] = temp_idx[[x for x in temp_idx if 'date' not in x]].apply(create_index)

df_rev_index_dict[key] = temp_idx

# Create train/test dataframes

df_rev_train_dict = {}

df_rev_chg_train_dict = {}

df_rev_test_dict = {}

for key in df_rev_index_dict:

# Create ticker list

tickers = [x.lower() for x in sector_dict[key]]

# Create dataframe fo all

df_out = df_rev_index_dict[key]

# Base train df

df_train = df_out.loc[df_out['date'] < "2023-01-01"].copy()

df_rev_train_dict[key] = df_train

# Chang train df

df_train_chg = df_train.copy()

df_train_chg[tickers] = df_train_chg[tickers].apply(lambda x: np.log(x).diff())

df_train_chg = df_train_chg.dropna()

df_rev_chg_train_dict[key] = df_train_chg

# Test df

df_rev_test_dict[key] = df_out.loc[df_out['date'] >= "2023-01-01"]

# Forecast comparison

y = df_rev_train_dict['xlk']['aapl']

y_act = df_rev_test_dict['xlk']['aapl']

hist_dates = df_rev_train_dict['xlk']['date']

forecast_dates = df_rev_test_dict['xlk']['date']

# Fit ETS model: Error='add', Trend='add', Seasonality='add'

ets = ETSModel(

y,

error='add', # 'add' or 'mul'

trend='add', # 'add', 'mul', or None

seasonal='add', # 'add', 'mul', or None

seasonal_periods=4

)

fit = ets.fit(disp=False)

forecast = fit.get_prediction(start=16, end=19)

# # Get the last value of y to connect predictions and actual

last_y_value = y.iloc[-1]

last_y_date = hist_dates.iloc[-1]

# Plot

plt.figure()

# Plot historical data

plt.plot(hist_dates, y, 'b-', label='Historical', linewidth=1.5)

# Plot fitted values

plt.plot(hist_dates, fit.fittedvalues, 'g-', label='Fitted', linewidth=1, alpha=0.7)

# Plot actual test values connecting to last historical value

plt.plot([last_y_date] + list(forecast_dates),

[last_y_value] + list(y_act.values),

'k-', label='Actual Test', linewidth=1.5)

# Plot forecast values connecting to last fitted value

last_fitted_value = fit.fittedvalues.iloc[-1]

plt.plot([last_y_date] + list(forecast_dates),

[last_fitted_value] + list(forecast.predicted_mean),

'r--', label='Forecast', linewidth=1.5)

# Add vertical line to separate historical and forecast periods

plt.axvline(x=last_y_date, color='gray', linestyle=':', alpha=0.5, label='Forecast Start')

plt.title('Revenue Forecast with Historical and Test Data')

plt.xlabel('Date')

plt.ylabel('Indexed Revenue')

plt.legend(loc='upper center', ncol=5)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Get error

ets_rmse = np.sqrt(np.mean((y_act - forecast.predicted_mean)**2))

ets_rmse_scaled = ets_rmse/y_act.mean()

# Auto ETS

fh = np.arange(1,5)

auto_ets = AutoETS(

auto=True,

n_jobs=-1, # 'add' or 'mul'

sp=4

)

auto_ets.fit(y)

y_pred = auto_ets.predict(fh=fh)

# Plot

plt.figure()

# Plot y with historical dates

plt.plot(hist_dates, y.values, 'b-', label='Historical', linewidth=1.5)

# Get the last value of y to connect predictions and actual

last_y_value = y.iloc[-1]

last_y_date = hist_dates.iloc[-1]

# Plot y_act connecting to last y value

plt.plot([last_y_date] + list(forecast_dates),

[last_y_value] + list(y_act.values),

'g-', label='Actual', linewidth=1.5)

# Plot predictions with dashed lines, starting from the last y value

plt.plot([last_y_date] + list(forecast_dates),

[last_y_value] + list(forecast.predicted_mean),

'r--', label='ETS Forecast', linewidth=1)

plt.plot([last_y_date] + list(forecast_dates),

[last_y_value] + list(y_pred.values),

color='purple', linestyle='--', label='AutoETS Forecast', linewidth=1)

plt.axvline(x=last_y_date, color='gray', linestyle=':', alpha=0.5, label='Forecast Start')

plt.legend(loc='upper center', ncol=5)

plt.title('ETS and AutoETS Revenue Forecasts Comparison for AAPL')

plt.xlabel('')

plt.ylabel('Indexed Revenue')

plt.show()

# Get error

autoets_rmse = np.sqrt(np.mean((y_act - y_pred)**2))

autoets_rmse_scaled = autoets_rmse/y_act.mean()